A financial model investigating the issuance of digital money as central bank

digital currency (CBDC) or privately as stablecoins found that a

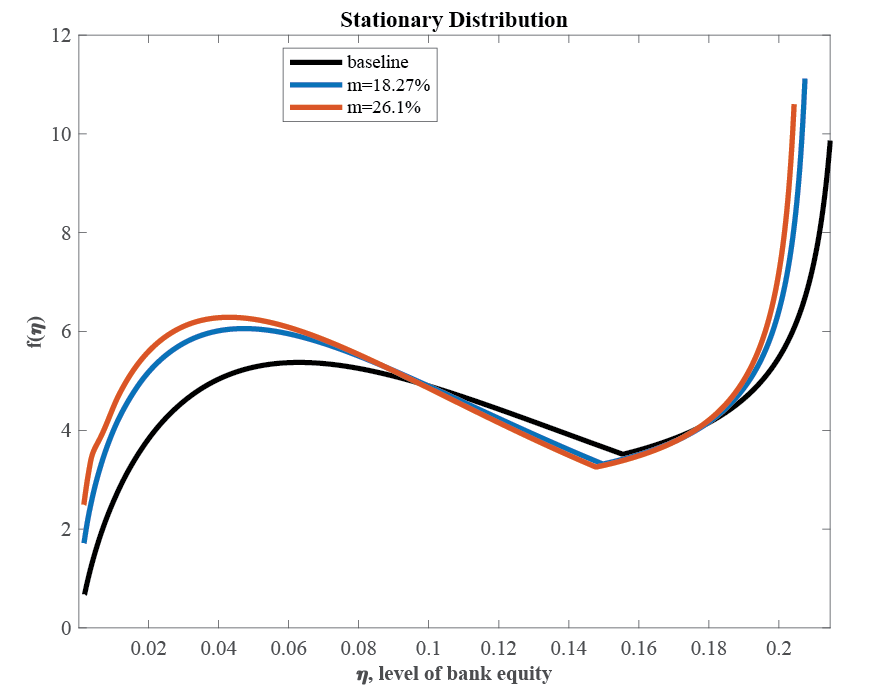

fully-integrated digital currency would lead to higher and less volatile asset

prices, and household welfare gains are potentially large which could lead to an

increase in consumption by up to 2%. However, a fully-integrated digital

currency would depress bank deposit spreads, particularly during times of

crises, which limits the banks’ abilities to recapitalize losses after a bank

crises. These investment losses, not specifically bank runs, create instability,

the paper argues. Another research paper found that bank runs are not as big as

initially feared. This paper can be found here:

https://www.financialresearch.gov/working-papers/2022/07/11/central-bank-digital-currency/

[https://www.financialresearch.gov/working-papers/2022/07/11/central-bank-digital-currency/]

Both papers focus on the issuance of CBCD and stablecoins and do not include

privately issued money like LETS/Time Dollars and similar privately issued

complementary currency systems.