- cross-posted to:

- nyt_gift_articles@sopuli.xyz

401ks weren’t a “mistake” they were designed to give wallstreet traders more money and for that task they have succeeded extremely well.

e: To the tune of $7trillion according to the article.

Maybe giving a percentage of your income to legal gambling is a bad idea???

What else do I do? Put that money under my mattress?

No, put it under my mattress

A highly diversified portfolio is the opposite of gambling. Don’t let the “traders” and crypto bros sour you on the power of conservative investing.

So what I’m saying is: the money you put into a 401k goes to an investment company, that investment company gambles in the stock market.

Regardless of how you spin it, regardless of how safe you think it is, when you give money to someone to use in the stock market you are gambling.

No, diversification makes it not gambling. Not all risk is gambling.

lol…any time you give money to someone else to manage you are gambling.

Making a assumption that your money will increase in value over x is (say it eith me) gambling…otherwise why would those guys in suits have disclaimers saying “you may lose money…not all accounts make money…etc…”

I mean, by all means go ahead, if this makes you happy go right ahead. My point still stands.

It’s not an assumption, I understand the risks. I know it will go both up and down. That doesn’t make it gambling. What on earth isn’t gambling in your eyes?

death and taxes. sure bet.

understanding of risks doesn’t cut the mustard… I understand the house always wins. Understanding the odds in blackjack and understanding the odds in the stock market still makes you a gambler…an informed gambler, but nonetheless a gambler.

So if 401ks are bad because they incentivize gambling, what’s the alternative? You have a uselessly broad definition that seems to lead people only to a guarantee of losing purchasing power through inflation. Better guarantee a loss than “gamble” with strong evidence to support your risk I see.

Saying “the house always wins” about things like index investing is hilarious.

You can direct your funds to money market accounts usually as well

No, the article is actually saying that people have not done this enough. Workers were better off when their employees did so for them and mandatorily (a pension system), and allowing folks to self manage how much they put away is what has led to 49% of folks within 10 years of retirement having nothing to retire on.

There are very safe ways to invest. Doing it poorly and a lot is a gamble; taking a little time to understand different investment vehicles and portfolios and the risks associated with each allows you to earn interest at literally any level of risk. An example, money market funds earned 5%-8% on 2023, and it is literally impossible for MMFs to go negative. Certified deposits offered up to 5.5% guaranteed returns. The benefit of pensions is that employees don’t need to learn all that and make those choices in order to benefit from them.

Putting a percentage of your income in the stock market is a very good idea. Even if you’re a conspiracy person and you think a mysterious “them” controls the world, “them” are rich people who own stocks. They will make sure the value of stocks go up.

If you’re not a conspiracy person, just look at history. The value of stocks always goes up in the long term, and you hold retirement accounts for the long term.

Maybe don’t encourage people to save in a currency that’s purposely depreciating throughout their entire lives?

Is there a currency that doesn’t depreciate?

Gold… Okay, well technically it inflates by 1.8% per year, but at least that’s steady and predictable. Where some years the dollar inflates by 3% a year and some years it inflates by 10%.

So the solution to 401k inequity is employer-sponsored gold reserves? I think just returning to a pension system probably works…

(Nor are any of the issues with 401ks mentioned in the article related to inflation)

I don’t know if a pension system would work as it seems like pensions were primarily for people who stayed for 20 years at one single job and nobody really does that anymore. But employers giving their employees gold wouldn’t be a bad thing. The article did not mention inflation, but it is a serious downside to a 401k. As an example, in 40 years, any money you save now will be worth 20% of what it currently is worth. If you save $100 at age 20 in a 401k, then by the time you are 65, that $100 would be worth something like $10 in today’s purchasing power. That’s an incredibly dumb thing to save in.

Except that 401ks are invested. By default they tend to be invested in a relatively stable, diverse portfolio along the standard long-term investment guidelines of ~60/40 balance of stocks and fixed or cash holdings. Mine made 15% last year invested even more conservatively than that, and it’s a no-name 401k provides by my small employer. I would have made significantly less with gold.

If you think people’s 401ks are just sitting there in a low-interest checking account, I don’t think you understand how they’re actually structured.

Oh, I understand. I get that the money is invested in things that will grow over time, but you’re still having to take risk in order to get that return. Otherwise, what happens is you lose your money to inflation. At least with gold, it’s a steady rise and will not fluctuate a whole lot. Gold holds your purchasing power with very little risk at all.

You’d find very few financial advisors or experts who would recommend putting your retirement portfolio entirely in gold.

Okay, well technically it inflates by 1.8% per year, but at least that’s steady and predictable.

Where are you getting that info from? The price and value of gold is insanely volatile, its value often changes based on people’s confidence in fiat currency.

Gold doesn’t have an inherent value, and is just as easily manipulated by governments as fiat currency. FDR changed the value of gold to print more money to sustain the recovery after the depression.

World gold council

Real estate?

Even if there was, there’s no currency that is guaranteed to not depreciate in the future.

This is the best summary I could come up with:

From the extensive research that she has done, Forbus has become a fairly savvy investor; she’s familiar with all of the major funds and has 60 percent of her money in stocks and the rest in fixed income, which is generally the recommended ratio for people who are some years away from retiring.

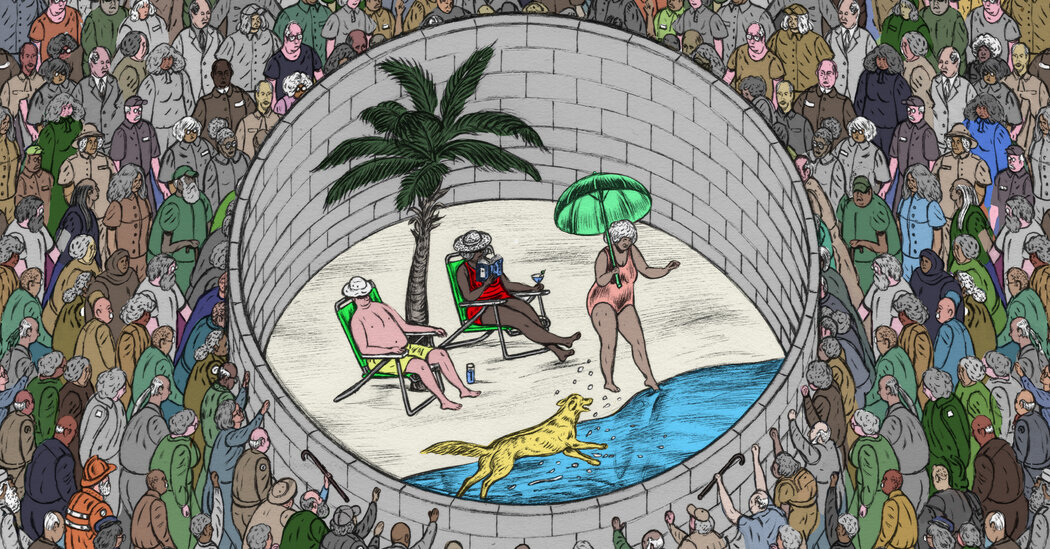

With Americans now aging out of the work force in record numbers — according to the Alliance for Lifetime Income, a nonprofit founded by a group of financial-services companies, 4.1 million people will turn 65 this year, part of what the AARP and others have called the “silver tsunami” — the holes in the retirement system are becoming starkly apparent.

But he explained to me that the remorse he expressed had nothing to do with 401(k)s themselves, which he said had helped convert millions of Americans from “spenders into savers.” Rather, what he regretted was the complexity of many plans — he thought a lot of employees were overwhelmed by all the investment options — and the fact that the financial-services industry profited from them to the degree that it did.

A few years ago, Kevin Hassett, who was chairman of the White House’s Council of Economic Advisers for a portion of Donald Trump’s presidency, became familiar with Ghilarducci’s work and sent her, unsolicited, the draft of a paper he was writing about the retirement-savings gap.

This past January, another bipartisan collaboration — between Alicia Munnell, who was an economist in the Clinton administration and who now serves as the director of Boston College’s Center for Retirement Research, and Andrew Biggs, a senior fellow at the American Enterprise Institute, a conservative think tank — published a paper calling for a reduction or an end to the 401(k) tax benefit.

Hassett has been concerned for some time that the country is drifting toward socialism — the subject of his most recent book — and part of the reason is that too many Americans are economically marginalized and have come to feel that the system doesn’t work to their benefit.

The original article contains 4,649 words, the summary contains 341 words. Saved 93%. I’m a bot and I’m open source!