{kind=link}

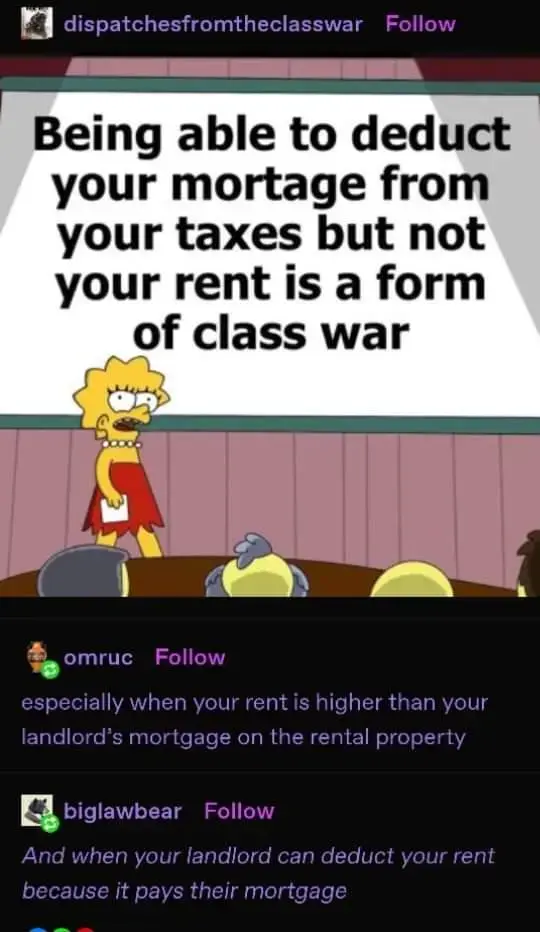

In the US you can deduct the mortgage interest, which is even more of a benefit for the wealthy than the mortgage as a whole would be since the deduction decreases the longer someone stays in a home.

Social security being a flat percentage with a cap is also a form of class war.

Investment income being taxed less than employment income is another form of class warfare.

Why the hell do you pay more in taxes than Elon Musk?

Are you talking about capital gains tax?

First, let’s be clear, the reason the rich pay little tax doesn’t have much to do with the capital gains tax rate being lower.

Now the reason for the lower rate (at least ostensibly) is that while income is earned at a point in time, capital gains happens over large amounts of time. Therefore often a big part of the gain is inflation. Let’s imagine you bought a house for $100k and 20 years later you sell the house for $140k. Over that time inflation has been a steady 2%.

Due to inflation $148k is now worth what $100k was worth 20 years ago. But when you sell you have to pay tax on the $40k profit even though you actually made a loss?

Lower capital gains rates are meant to adjust for this. Basically saying we understand part of the gain is inflation, so let’s call it half inflation and half profit and we’ll account for this by setting the capital gains rate at half the income tax rate.

Remember companies (that you might have shares in) or yourself as a land lord are (ostensibly) paying tax on profits as you go. Capital gains tax is in addition to this.

This comment is already long enough so I’ll leave the conversation on whether this stuff is true in practice as an excercise for the reader, but it at least starts from a sensible place.

At least where I live (not the US), if you’re day trading stocks or flipping houses you’ll pay income tax not capital gains tax (ostensibly 😆).

There’s nothing stopping people in the lower classes from investing.

If minimum wages are so low and working hours so long that people are too busy with their day jobs and/or don’t make enough money to even think about the stock market, let’s focus on fixing that rather than going after the stock market.

There’s nothing stopping people in the lower classes from investing.

Bwahahahahaha

I think an argument is that because many people live paycheck to paycheck, investing simply isn’t an option. Many costs in life are somewhat fixed — I buy similar groceries compared to someone who makes half what I make, and compared to someone who makes twice what I make; as a fraction of income it’s a huge spread.

What this means is that making twice as much money doesn’t mean you get to invest twice as much — you can invest way more, because the difference in income is largely disposable.

Or how about we don’t subject companies to the enshittification whims of rich assholes and base our entire society’s worth on some arbitrary values on a computer screen? If you want to gamble on line go up or down, fine, but let’s divest it from how we govern our lives, because clearly it isn’t working for the majority of us.

Hahaha!

Why don’t these peasants simply become landed gentry? Rather than worrying about feudalism, they should worry about establishing their dynasty.

Holy shit what an idiotic thing to say.

It may surprise you to find out that “lower class” people are in the lower class because they don’t have money. What are they supposed to invest?

There’s nothing stopping people in the lower classes from investing.

except for the whole being poor thing

Trolls of Lemmy, you can pack your bags. You will never be able to come up with something dumber than this.

I’m honestly not sure if it’s trolling, or satirizing the trolls. It could go either way.

Poor people can easily find out about SPY. The issue is not the amount of time.

Yup, and all of these are sold as benefitting the non-wealthy while glossing over how much more it benefits the wealthy.

I don’t follow why the mortgage interest is better for the wealthy than the total mortgage amount?

In the USA afaik it is only the interest which is tax deductible.

Rich people can buy high end homes that they know will appreciate in value, and their interest rate will be lower because they are wealthy. So if they get a good enough rate they are basically getting a tax break for what they are paying for the house and then selling it for more profit. They can do this because they are wealthy enough to decide on when to make large transactions.

As a deduction it will have a far higher impact on their taxes because whatever the amount is paid in interest is coming out of their highest tax bracket.

So if they are paying 10k in interest on a more expensive house becsuse rheir interest rate is lower and the 10k reduced their income taxed at 20+% they will get a far bigger benefit out of it than someone paying 10k at a higher interest rate that might lower their income taxed at 10% and when they sell their house they will get less of an increase from it.

Not sure I get why social security being flat with a cap benefits one class over the other.

Sure, once I meet the max contribution then my withholding goes down and my take home increases. But anything in excess of the max contribution doesn’t affect social security payouts after retirement — if you put in more, you get out more, and if you’re capped in your contributions then you’re also capped in your withdrawals.

Is it a paternalistic program? Sure, it’s essentially a forced retirement plan. Its implementation isn’t perfect, but I’m not sure I’d call it class warfare.

When wealth is concentrated because wages don’t increase with productivity, the wealthy are paying less than their fair share of taxes to society with a flat percentage that has a cap.

Look at it this way, if there is 1 million dollars taxed at 3% and there is no cap it doesn’t matter who gets what, $30k total is collected. If there is a 100k cap and one person takes in 500k and 10 people take in 50k in income apiece then only $9k is collected and the one taking in 500k is putting in the same amount as everyone else. They are also less in need for social security retirement savings because they can easily squirrel away more in savings.

Yes, the taxation is regressive, but the benefits are progressive. E.g.,

According to the non-partisan Congressional Budget Office, for people in the bottom fifth of the earnings distribution, the ratio of benefits to taxes is almost three times as high as it is for those in the top fifth.

( https://en.m.wikipedia.org/wiki/Social_Security_(United_States) )

It’s certainly not a perfect system, but personally I think it has some merit. And it’s by far not the worst aspect of USA tax structure (in my opinion).

You can’t deduct your mortgage from your taxes, only the interest. And only on mortgages related to your first or second home. From irs.gov

This part explains what you can deduct as home mortgage interest. It includes discussions on points and how to report deductible interest on your tax return.

Generally, home mortgage interest is any interest you pay on a loan secured by your home (main home or a second home). The loan may be a mortgage to buy your home, or a second mortgage.

Another important thing to note is that you only benefit from this if you have so many itemized deductions that you can do better than the standard deduction. The mortgage interest alone isn’t going to do that in a vast majority of cases. Since legislation in 2017, a lot of the tax advantage of owning a home was reduced.

The OP is wrong on every conceivable level.

Yeah. To break down why this meme is bad information, in simple terms:

- You can’t deduct “your mortgage”. You can only deduct interest on a loan.

- You can’t take this deduction on a rental property. You have to live in the home part of the year to take this.

- Since the tax changes in 2017, most homeowners don’t deduct mortgage interest anymore, because it’s better to take the standard deduction offered to anyone.

Don’t share or believe bad information.

Oops, sorry

There’s actually a few types of interest, including student loan, that can be deducted.

The mortgage tax advantage is just one component of it.

After WWII we made (mostly suburban) homes be retirement investment vehicles for (almost exclusively white) working class people. That was a terrible choice for all future generations of the working class. Now most people (white or not) are priced out. It’s been great for the boomers and the real estate & finance industries, though, thanks to asset price inflation.

From Michael Hudson’s Killing the Host (PDF):

The Bubble Economy vs classical industrial growth

The stock market is not the largest part of the economy whose prices are inflated by bank credit. As the biggest asset category, real estate is by far the largest market for debt. The Federal Reserve’s quarterly Flow of Funds statistics show that by 2007-08, about 80 percent of new bank loans were real estate mortgages. Most such loans are to buy property already in place, just as most stock market transactions are for shares long since issued.

The effect is twofold: it inflates asset prices ranging from real estate to entire companies, and yields banks interest that imposes a carrying charge on buyers. That is what makes bubble economies high-cost. Housing prices are inflated, requiring mortgage debtors to pay more. Companies borrow to buy other companies, increasing the volume of corporate debt simply to finance ownership changes. And education is financialized, enabling students to afford higher tuition costs by committing to pay monthly debt service out of what they earn after they graduate.

The resulting financial overhead consists of claims on the economy’s actual means of production. Yet most people think of these bonds, bank loans and stocks and creditor claims as wealth, not its antithesis on the debit side of the balance sheet. This inside-out doublethink is a precondition for the bubble economy to be applauded by the mass media, keeping its corrosive momentum expanding.

From the corporate sphere and real estate to personal budgets, the distinguishing feature over the past half-century has been the rise in debt/ equity and debt/income ratios. Just as debt leveraging has hiked corporate break-even costs of doing business, so the cost of living has been increased as homes and office buildings have been bid up on mortgage credit. “Creating wealth” in a debt-financed way makes economies high-cost, exacerbated by the tax shift onto labor and consumers instead of capital gains and “free lunch” rent. These financial and fiscal policies have enabled financial managers to siphon off the industrial profits that were expected to fund capital formation to increase productivity and living standards.

Look look look as a home owner with a mortgage, I think you’re looking at this all wrong.

You should be furious and demanding correction French style.

It’s super wrong and political action is desperately needed

Just get a mortgage then -brought to you by the privileged

I have never deducted my mortgage on my taxes. Only a percentage of the property tax paid. If there is a way to deduct an entire mortgage i would love to know

Quiet, we’re trying to get mad at people we’ve never met over problems we made up over here.

Oops, my bad. Mums the word

I wish I could up-vote more than once…

Don’t forget to deduct your home office if you work from home.

Small business owners can deduct their home office, employees cannot

Source: https://www.irs.gov/newsroom/how-small-business-owners-can-deduct-their-home-office-from-their-taxesI was just officially classified as a remote employee in my company’s HR system, even though I’ve technically been working more at home than in the office since the pandemic. How exactly do I measure how much I should be deducting because of my home “office”?

Unfortunately that deduction is for small business owners, not employees.

Source: https://www.irs.gov/newsroom/how-small-business-owners-can-deduct-their-home-office-from-their-taxesMore context: I’m a full-time remote employee :')

Wait, can you do this in Canada? If so I haven’t been for the last 9 years.

Also Canadian, and if we can do this I’ve been missing the fuck out for decades.

It’s the other way around in Quebec, Ontario, and Manitoba, isn’t it?

In Minnesota, the part of rent that pays property taxes is deductible if one’s income is not high. https://www.revenue.state.mn.us/renters-property-tax-refund

Same for NJ

Though, it’s not like one’s state return is typically impressive…

Mortgage tax deductions are nothing more than a check from the tax payers to the banks. And the banks take the deductions into account for how much interest they can ask. So homeowners pay the same amount as if those deductions didn’t exist. Also they do nothing for affordability if not more homes are build. The advantage you get is already calculated into the price of the home. It just increases demand and thus raise the prices of homes.

Ignorance defined. Mortgage interest is completely different than rent.

So ignorant

Wait, sorry, wrong kind of Class War.

In the USA at least, this is false. Rent is your Landlord’s Income, so they always have to report it as such. They can write off depreciation of assets but not mortgage. They can deduct mortgage interest, though.

AND you also have to pay Capital Gains taxes on sold real estate unless the property was used solely as your main residence for several years.